- Jun 4

May 2026: How the Account Performed: SPX Recovery, Adjustments, and a Strong SPY Ride Close

- Pedro Branco

- 0 comments

By Pedro Branco | MyOptionsEdge

May 2026 was a recovery month for the market and for the account. After a difficult April that saw SPX drop nearly 10% from its January highs and the VIX spike into the low 30s, May brought a sustained market recovery, declining implied volatility, and a return to the kind of environment where non-directional premium-selling strategies do exactly what they're designed to do.

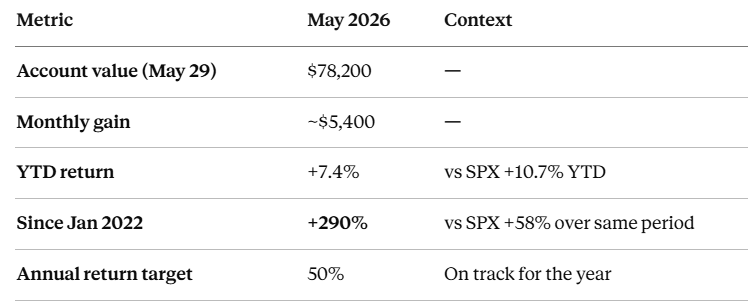

The fund closed May at $78,200, a gain of approximately $5,400 for the month, bringing the YTD return to +7.4%. The since-inception return since January 2022 now stands at +290%, compared to SPX +58% over the same period.

It wasn't a simple month. A strong directional market move upward created an above-average number of adjustment decisions across both the SPX Best and Ride Trade positions. But the core thesis held: maintain positive Delta bias, let IV contraction work in our favour, and manage positions rather than panic-close them.

The numbers

SPX has outperformed the fund on a YTD basis through May, the market's strong recovery from the April lows produced gains that a non-directional strategy captures only partially. That's expected and by design. The fund's edge shows most clearly in the full cycle, including periods like April 2026 when SPX fell and the fund held up significantly better than the index.

The +290% since January 2022 versus SPX +58% tells the complete story across bull markets, a bear market, volatility spikes, and low-IV periods. That four-year track record is publicly available on the Trading Account page. every month, no gaps.

What drove the May gain

SPX Best Trades: positive Delta bias paid off

The SPX Best positions were the primary driver of the month's gain. Entering May, all three open positions — with June, July, and later expirations — were managed with a positive Delta bias. This was a deliberate decision based on the market thesis: the April correction appeared complete, the TOY and January Barometers were both bullish for the year, and the probability-weighted scenario called for SPX to recover toward new highs by year-end.

That bias was tested in May. The market moved up strongly (and "strongly" in this context means more than a gentle drift). It was a directional move that required multiple adjustments across all three SPX Best positions to maintain the appropriate Delta balance and keep the structures in their profitable zones.

The adjustments worked. The combination of positive Delta exposure capturing the upside move, together with IV contraction as the VIX declined from elevated post-April levels, contributed meaningfully to the month's gain.

At month-end, three SPX Best positions remain open:

18 JUN expiration: final weeks of the trade, monitoring closely (should be closed for a nice profit in the first week of June)

30 JUN expiration: mid-trade, in positive territory

17 JUL expiration: early stage, well-positioned vs SPX price

All three are working as expected entering June.

SPY Ride Trade — closed for ~$1,900 profit

The highlight of the month was closing a SPY Ride Trade for approximately $1,900 profit; the largest single trade close of 2026 so far.

The Ride Trade is a calendar spread structure on SPY that benefits from positive Theta and positive Vega simultaneously. It's the natural complement to the SPX Best, where the SPX Best is Vega negative (benefits from IV contraction), the Ride Trade is Vega positive (benefits from IV expansion). Running both simultaneously is the portfolio construction approach that smooths returns across different market regimes.

The May close captured the final IV contraction as volatility normalised after the April spike. The Ride Trade had been adjusted multiple times during the month (more than average) as the strong upside move in SPY required Delta management. The adjustments were more frequent than a typical Ride Trade month, which is the honest reality of managing calendar spreads through a strong directional move. But the underlying thesis was correct and the position closed profitably.

A new SPY Ride Trade position is currently open with unrealised profit entering June.

SPX Quants — new position opened with a good start

In the final week of May, a new SPX Quants trade was opened. The SPX Quants strategy uses vertical spreads to capture directional moves in the S&P 500 based on quantitative signals. This is a shorter-term, higher-Delta strategy that complements the non-directional SPX Best and Ride Trade positions.

The position was opened in response to a specific quant signal and currently sits at a nice unrealised profit entering June. Full details of the entry rationale and position structure are documented in the Trading Community.

The honest part: more adjustments than usual

I always include this section because it's the most useful part of a performance post: not the wins, but the challenges.

May delivered an above-average number of adjustment decisions for both the SPX Best and Ride Trade positions. The reason was the market's directional behaviour: SPX moved up strongly and continuously for much of the month, creating persistent positive-Delta drift in the SPX Best structures and negative-Delta pressure on the Ride Trade calendar spreads.

Managing these adjustments required more active monitoring than a typical month. In a range-bound or slowly trending market, the SPX Best and Ride Trade run largely on autopilot between weekly check-ins. In a strongly trending month like May 2026, the positions required more frequent attention to maintain the Delta targets and keep the structures within their intended zones.

This is not a problem. It's the strategy working as designed. Adjustments are how discretionary positions adapt to changing market conditions rather than taking maximum losses. The cost is time and mental energy. The benefit is that positions stay manageable even when the market doesn't cooperate with the initial setup.

What I'd do slightly differently: on the Ride Trade specifically, I could have been slightly more aggressive with the first adjustment when the move began. Waiting a day or two longer than optimal before rebalancing Delta. The outcome was still a $1,900 profit, but the path could have been smoother. This is the kind of judgment refinement that only comes from executing these positions through many market cycles.

What the market looked like in May

After the April correction, which took SPX from near all-time highs down approximately 9.6% peak-to-trough, May was a recovery month with genuine conviction behind it.

Several quant factors supported the bullish case throughout May:

Momentum thrust signal: For the first time in 28 years, SPX had stayed above its 10-day moving average for 22 straight days while gaining 10%+. Forward returns following this setup have been positive every single time over the next one to six months in the historical record.

VIX normalisation: The VVIX (volatility of volatility) fell back below where it started 2026, confirming that the panic phase of the April correction was complete. Historically, when volatility cools after an extended elevated phase with SPX near all-time highs, the S&P 500 has been higher four weeks later 9 out of 10 times.

Year-end setup: When SPX closes April at a new all-time high monthly close, the remainder of the calendar year has never been negative since 1950. A perfect 17-for-17 record, averaging +10.35% for the rest of the year.

For premium sellers, May's IV environment was the ideal sequence: elevated IV at the start of the month (from the April spike), providing good entry premium, followed by gradual IV contraction as the market recovered. That's exactly the environment the SPX Best and Ride Trade are designed to exploit.

Entering June: what the positions look like

Open positions at June 1:

SPX Best — 18 JUN: Final week. Monitoring for profit target or close decision before expiration. This trade has been through multiple adjustments and is in positive territory.

SPX Best — 30 JUN: Mid-trade. Positive Delta bias maintained. Structure well-positioned, assuming continued SPX stability or upside.

SPX Best — 17 JUL: Early stage. Clean entry, good structural positioning.

SPY Ride Trade: Open with unrealised profit. Calendar spread positioned for a continued low-IV environment.

SPX Quants: Short-duration directional trade opened late May. In unrealised profit entering June.

The June market context:

VIX is back in the 17–18 range, a moderate implied volatility, not historically low but not elevated. The IV Weekly's market thesis entering June calls for continued upside through the summer, with the annual SPX ATH likely forming in November or December. The current portfolio positioning (positive Delta across SPX Best positions, positive Vega via the Ride Trade), aligns with this thesis.

The 18 JUN position will be the first major decision of June. Watch for the trade close post in the Trading Community when it reaches the profit target.

The bigger picture: 2026 in context

Seven months into 2026, the fund is +7.4% YTD against SPX +10.7%. The market has outperformed the fund on a raw YTD basis, which due to our +Delta conservite bias, having a strong recovery year and where the index bounced aggressively from the April lows.

What the YTD number doesn't capture: the fund was significantly ahead of SPX during the April correction. When SPX was down -5% or more YTD in March-April, the fund was holding up materially better. The non-directional structure absorbs drawdowns more effectively than a passive index position, which means the full-year comparison at December 31 is the relevant measure, not the mid-year snapshot.

The 50% annual return target remains the goal. At +7.4% through May, the pace is below the target run rate for the year. June through December. Historically strong months in a year with the quant setups described above will be where that gap closes. The fund has delivered +30–48% in each of the previous three full calendar years. The setup for the second half of 2026 is among the most constructive we've seen since 2021.

Follow along in real time

Every trade described in this post (the SPX Best adjustments, the Ride Trade close, the Quants entry) was documented in the Trading Community as it happened. Not in a monthly summary written after the fact, but live: the entry rationale, the brokerage screenshot, the adjustment logic, and the close post with full P&L.

June's trades are already being posted. The 18 JUN SPX Best is in its final weeks. The next SPX Best opening, whenever conditions are right, will be posted the moment it's placed.

If you want to follow these trades in real time rather than reading about them at month-end, the 15-day free trial is the place to start. You'll see everything (every position, every adjustment, every weekly IV analysis) before committing to anything. Or If you're wondering what the path to generating this kind of consistent income actually looks like, I wrote a detailed 12-month roadmap that covers exactly that → Options Trading for Monthly Income: A Realistic 12-Month Roadmap.

👉 Start your 15-day free trial — full Trading Room access, live SPX Best and Ride Trade trades, weekly market research. No commitment before day 15.

👉 View the complete fund performance record — every month since January 2022, publicly documented.

Past performance is not indicative of future results. Options trading involves significant risk and is not suitable for all investors. All performance data shown is from a real account and is publicly documented on the Trading Account page.

About the author: Pedro Branco is a volatility-focused index options trader who has traded options for more than 15 years and has run a live investment fund since 2020. The fund uses non-directional income strategies — the SPX Best broken wing butterfly, the SPY Ride Trade calendar spread, and the SPX Quants directional strategy — with every trade documented publicly. He is the author of The Volatility Trading Plan, available on Amazon.