The SPY Ride Trade is a non-directional options strategy built on three calendar spreads — designed to profit from time decay while keeping directional risk small and manageable. Target: 10–15% return per trade, typically achieved in 30–40 days. A delta-neutral income approach on the most liquid ETF in the market.

Verified monthly on the Trading Account page →

The course is sold as a subscription, including access to the trading Room.

You can learn and follow my Ride Trades by subscribing to the Trading Community.

What the Ride Trade is

The Ride Trade uses a structure of Calendar Spreads on SPY options, positioned to profit from two sources simultaneously:

Positive Theta — the position generates income from time decay. Time passing works in your favour from day one.

Positive Vega — the position benefits when implied volatility increases. An IV spike that would hurt many other strategies actually helps the Ride Trade — which is why it complements the SPX Best strategy (which is Vega negative) as a natural portfolio hedge.

This dual characteristic — profiting from both time decay and IV expansion — makes the Ride Trade particularly well-suited to low IV environments, where the SPX Best may produce thinner premium. The two strategies are designed to work together across all market conditions.

What "non-directional" means for the Ride Trade:

Like all my strategies, the Ride Trade does not require predicting which way the market will move. The calendar spread structure creates a wide price range where SPY can move — up, down, or sideways — while still generating a profit. Even in cases of larger moves, defined adjustment protocols manage the directional risk and keep the position working.

Key characteristics:

Structure: Calendar Spreads using Delta-based strike selection that adapts to market conditions at entry

Expiration selection: Longer-dated options chosen specifically to reduce volatility and minimise adjustment frequency compared to short-dated alternatives

Delta target: Near-neutral at entry, with adjustments made to maintain control as the underlying moves

Minimum account size: $5,000 suggested. Typical capital allocated per position: ~$4,500

Time commitment: 15–30 minutes per day to monitor. Adjustments average less than once per week outside of the final 50 DTE period

-----------------------------------------------------------------------

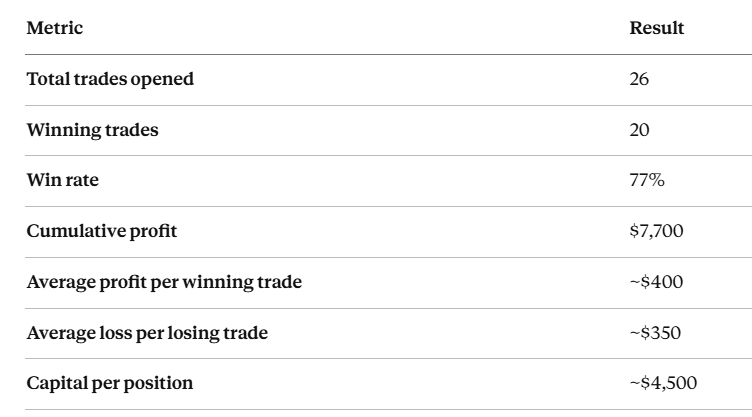

The performance data below reflects real trades in a real account — not backtested simulations.

2021 full-year performance (the most comprehensively documented period):

The Ride Trade is actively traded in my account alongside the SPX Best. The full monthly fund record is publicly available on the Trading Account page.

→ View the complete performance record

Most traders look for a single strategy to trade in all conditions. I've found that running the Ride Trade and the SPX Best simultaneously gives the portfolio a structural advantage:

The SPX Best is Vega negative, it benefits from IV contraction and high IV at entry

The Ride Trade is Vega positive; it benefits from IV expansion and low IV at entry

This means when market conditions favour one strategy, they often provide a hedge for the other. In practice, I typically have 1 Ride Trade positions and 3 SPX Best positions open simultaneously at different expirations, creating a balanced, income-generating portfolio that works across all market regimes.

This is not a coincidence. It's a deliberate design of the fund's portfolio construction.

Every SPX Best position I open goes into the Trading Room the moment I place it — with the full rationale, the strikes, the payoff diagram, and the brokerage screenshot. The next trade will be there. So will every adjustment. So will the close.

The best way to learn this strategy is to watch it happen in real market conditions, alongside the community, with every decision explained as it's made.

👉 Start my 15-Day Free Trial Full Trading Room access · Live SPX Best trades · Weekly IV research · Cancel anytime

👉 Want to learn the SPY Ride Trade properly? This plan: $99/mo for flexibility, or $899/yr (save 24% — about $74/mo).

👉 Join Core Fund Strategies ($1,799/yr) Full SPX Best course + SPY Ride + VXX Short Call + 12 months Trading Room