Sign up to receive my Weekly Market Thesis that includes Market Research, S&P Quant Data, Promotions and Educational Options tips. Exclusive for subscribers

The best definition of VXX I have ever seen is given on sixfigureinvesting.com blog: VXX is a dangerous chimeric creature; it’s structured like a bond, trades like a stock, follows VIX futures and decays like an option. Handle with care!

If you want to move to a real-life example of a trading strategy using this VIX Short-Term Futures ETN, I am disclosing it for free. This is an options trading strategy with limited risk using exclusively VXX options: VXX FREE Options Strategy.

Going into its definition, VXX is a volatility product (exchange-traded note or ETN) designed to give traders exposure to changes in the VIX Index through near-term VIX futures contracts (/VX). Traders who buy VXX are anticipating an increase in the VIX Index or futures, while trades who sell VXX are anticipating a decrease in the VIX Index/futures! But, it is not exactly like this.

The VIX Index is not tradeable in the financial markets. It is a computed figure that measures a constant 30-day weighting by using multiple SPX options expiration cycles, as stated by CBOE:

"Only SPX options with more than 23 days and less than 37 days to the Friday SPX expiration are used to calculate the VIX Index. These SPX options are then weighted to yield a constant, 30-day measure of the expected volatility of the S&P 500 Index."

Let’s check both charts side-by-side where you can conclude that VXX does not mirror exactly the VIX index.

You can observe that, although they are highly correlated, VXX is losing value as time passes, unlike VIX which shows an horizontal price movement. Like an option, it has some "time decay". It can be easily noted in this small chart period of 4 months. Check below the chart for the past 3 years…

VXX tracks the S&P 500 VIX Short-Term Futures Index, which tracks the first and second-month VIX futures contracts, as stated by Barclays Bank PLC:

"S&P 500® VIX Short-Term Futures Index utilizes prices of the next two near-term VIX® futures contracts to replicate a position that rolls the nearest month VIX futures to the next month on a daily basis in equal fractional amounts. This results in a constant one-month rolling long position in first and second-month VIX futures contracts."

VXX's goal is to track the daily percentage change of a 30-day VIX futures contracts. Since there isn't a VIX futures contract with 30 days to settlement on each trading day, they use the first-month and second-month VIX futures to achieve a 30-day weighted VIX futures contract.

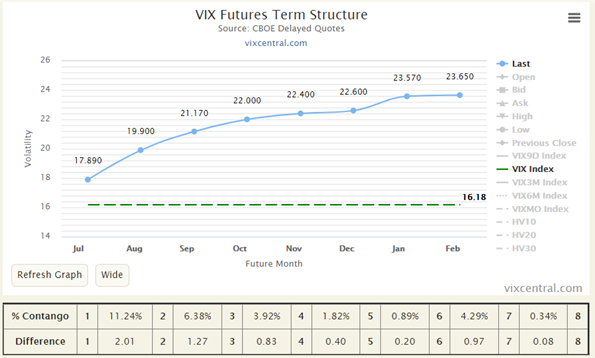

Below, you can see the structure of the VIX futures on 9 Jul 2019.

Every day Barclays Bank PLC is rolling a bit from the front month future to the following month. You can check the percentage of each one at their website: https://www.ipathetn.com/US/16/en/details.app?instrumentId=341408.

Under "normal" market conditions, the VIX futures structure is in Contango as the above chart illustrates. This is the “normal” market condition which is present around 80% of the time. So, if Barclays buys the second month (Aug) and sells the front month (Jul) (that it was already in their possession) will make the VXX value lose... they are buying high and selling low! And this is making VXX lose value.

Additionally, as time passes, there is another effect to consider. The futures will lose value also as time passes until they settle at spot VIX price (under normal circumstances, it will be lower than the front-month future). In the example above, if VIX does not move on Jul 20th (expiry date of the future), its value will be 16.18. Currently is at 17.89… since VXX is a long future holder, it will lose over time due to this effect (under normal market environment or in Contango).

If the first-month and second-month VIX futures decrease, VXX will lose value; conversely, If the first-month and second-month VIX futures increase, VXX will gain value.

Under "normal" market conditions, the VIX Index is typically below the near-term VIX futures contracts (under "contango"). As time passes, VIX futures contracts slowly converge towards the VIX Index. If the VIX Index is below the near-term VIX futures, the contracts will lose value over time, leading to losses in VXX. The majority of the time futures are in “contango” and VXX will lose value over time.

The above chart considers the past 10 years of price differentials between VIX futures and the spot VIX in about a trading period of one month (19 trading days).

The takeaway of the VIX futures prices are higher than the spot VIX and will converge to it. A normal month starts with the front-month VIX futures contract about 8-10% above the spot level of the VIX (and the second month around 16%).

It's important to understand that from VXX's inception date to maturity date, the product underwent numerous reverse splits to keep the product's price from reaching 0USD. Currently, it is around 15USD and soon we would expect another reverse split (x4). Lower values of VXX are harder to trade, especially in more complex strategies like the “CROC Trade” where we want to capture the premium.

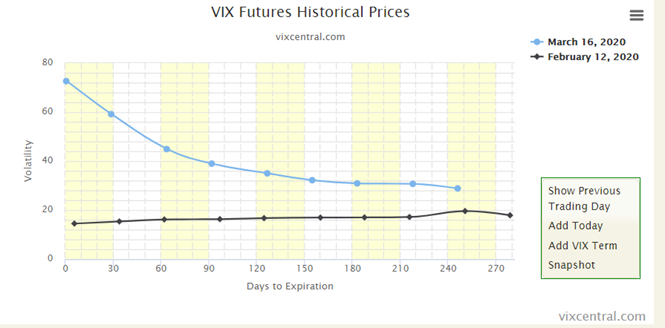

By opposition, when the VIX Index is above the near-term VIX futures (called "backwardation"), the contracts will gain value over time, which leads to an appreciation in VXX. This is not as usual as “contango”! Below an example where the VIX futures revert when we were at the peak of the Covid market crisis:

Under this "not normal situation", VXX has a "force" to... appreciate! the "contango" has now a negative value and is in "backwardation". If you read above how the VXX works, the situation here inverts and Barclays is selling higher-priced futures every day, rolling (buying) into lower-priced futures. In the example above they are selling at 42.375 and buying at 38.300. During these periods having long positions can pay-off... but it is not easy, as volatility has this "mean reverting" property and it can suddenly move down.

As being understood, VXX price changes can be violent, especially to the upside. When the market (SPY or SPX) start a violent move down (or a correction), the front two VIX futures can spike violently and VXX value will also move up. Trading VXX is considered risky and is part of a different asset class, which is Volatility trading.

Let’s have the example of the Covid crisis's impact on the Volatility space. In the below charts you have the price action from VXX, VIX and SPY (analysis period: mid Dec 19 until end of Mar 20). In percentage, it is computed the variation of each one from the bottom to its high.

As it can be easily concluded, the VXX can be a violent beast!

Let's also compare the VIX future structure curves before and during the crisis:

On Feb, 12th the VIX Futures market presented a curve was in Contango (it is not perceptible due to the scale after the violent futures move), with a value of 6%. On March 16th, at the crisis peak, backwardation was in place with a value of -19%! You can now see how violent the VXX moves can be... fortunately, these events do not occur often. But they do occur and we must expect that they can happen.

Another key takeaway from the analysis of these price movements is that the front month is more "elastic" (or reacts faster, than the following ones. On March 16th, spot VIX was above 80. This means the front month future was below with a value around 72. The futures market was completely reversed (or in Backwardation). This also impacts the price action of VXX which is more volatile than VXZ (another volatility ETN) that uses 6th and 7th future months.

As you understood VXX is a special asset with "time decay"... that can suddenly spike. So, trading this underlying with options needs special attention (like any other options strategy...).

I would start to advise how NOT to trade VXX:

1. Never (but never) sell naked Calls in VXX or any other volatility asset. This will have an infinite loss to the upside... in case of an unexpected volatility spike, you can have very big losses!

2. Negative Delta strategies tend to perform better in the long term because VIX futures are usually in Contango.

3. Do not buy VXX (or have high positive Delta options strategies); when VIX futures are in Backwardation you can have a Delta positive bias.

From VXX's inception date (January 2009) to maturity date (January 2019), the product lost 99.99% of its value because the VIX futures are usually in contango (circa 80% of the time). And that is why we can capture this value!

Nevertheless, we “should handle” with care because “Volatility take the stairs down, but the elevator up!”

Side note:

After the maturity of VXX (A Series, the first one to be launched), Barclays launched VXXB, which is essentially the same exact product that the original VXX was. In May 2019 Barclays renamed the VXXB back to its original ticker VXX. The only difference between the original and the new one that is being traded is the maturity: the original VXX had 10 years of maturity and the new one has 30 years. VXX ETN is widely traded, being very liquid along with its options. Market participants have now a high maturity product in the volatility trading space.