- Mar 13

How to Trade Iron Condor Options Safely: A Step-by-Step Guide for Consistent Profits

- Pedro Branco

- Iron Condor

- 0 comments

Key Takeaways

• Enter iron condors only when IV Rank exceeds 60-70, as high implied volatility inflates premiums and improves risk-reward ratios significantly.

• Target 15-25 delta short strikes and collect roughly one-third of wing width as credit to optimize the probability of profit.

• Close positions at 25-30% of maximum profit rather than holding to expiration to avoid late-stage gamma risk and assignment threats.

• Always adjust the untested side when the price approaches short strikes, rolling it closer to collect additional premium and widen breakevens.

• Limit individual iron condor positions up to 5% of portfolio capital and avoid trading during low volatility environments or short timeframes.

The key to iron condor success lies in systematic entry timing, disciplined profit-taking, and proactive position management. When executed properly with high IV entry conditions and mechanical adjustment rules, this strategy can achieve 70-80% win rates while generating consistent income from time decay and volatility contraction. What if I told you that iron condor strategies can deliver probabilities of profit between 80% to 90% when constructed well? Many experienced traders want a 70-80% success rate with this neutral options approach!

That's the power of trading iron condors in the right market conditions. Iron condor options are directionally neutral and defined-risk strategies that allow you to profit when the underlying asset stays range-bound. You benefit from time decay and decreasing implied volatility.

In this piece, I'll walk you through how to construct, manage and adjust your iron condor positions for income generation while avoiding the common mistakes that trip up most traders.

*****

What Is an Iron Condor Option Strategy

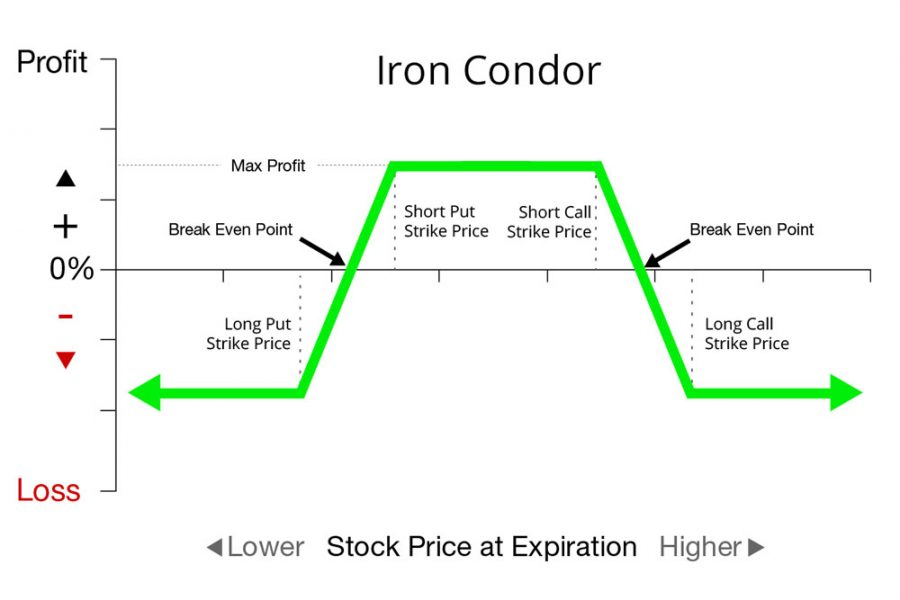

An iron condor is a four-leg options position that combines two credit spreads with the same expiration date. The strategy pairs a bull put spread below the current stock price with a bear call spread above it and creates a range-bound profit zone. This multi-leg approach allows you to collect premium upfront while limiting both potential profit and maximum loss through defined strike prices.

Components: Bull Put Spread and Bear Call Spread

The bull put spread forms the lower half of your iron condor. You sell an out-of-the-money put option at a higher strike price and buy another put at a lower strike price at the same time. This creates a net credit because the premium received from selling the higher-strike put exceeds what you pay for the lower-strike put. The spread profits when the stock price stays above your short put strike at expiration.

The bear call spread works in reverse on the upper side. You sell an out-of-the-money call option at a lower strike price while buying a call at a higher strike price. This also generates a credit, as the sold call brings in more premium than the purchased call costs. The bear call spread profits when the stock price remains below your short call strike.

Both spreads use the same underlying asset and expiration date. The long options in each spread serve as protection and define your maximum risk if the stock price moves against your position. Without this protection, you would face unlimited risk on the short options.

How Iron Condors Generate Income

Iron condors generate income through the net credit received when opening the position. You collect premium from selling both the put and call spreads, which represents your maximum profit potential. To cite an instance, if you receive a $2.00 credit per share when opening an iron condor, your maximum profit equals $200 per contract since each contract controls 100 shares.

The strategy capitalizes on three market conditions working in your favor. Time decay erodes the value of all four options each day, with the short options losing value faster than the long options. Minimal price movement keeps the stock within your profit zone between the short strikes. A decrease in implied volatility reduces option premiums across the board and allows you to buy back the position at a lower cost.

Your full credit is realized as profit if the stock price closes between the two short strike prices at expiration. All four options expire worthless in this scenario, and you keep the entire premium collected upfront.

Risk and Reward Profile

The maximum loss on an iron condor equals the width of one spread minus the net credit received. If you construct a $5 wide spread and collect a $1.50 credit, your maximum loss is $350 per contract: ($5.00 - $1.50) × 100 = $350. This maximum loss occurs when the stock price moves beyond either long strike at expiration.

Your position has two breakeven points calculated from the net credit received. The lower breakeven equals your short put strike minus the net credit. The upper breakeven equals your short call strike plus the net credit. Using the $2.00 credit example, if your short put sits at $100 and your short call at $110, your breakevens are $98 and $112.

The risk-reward ratio favors risk over reward. You might risk $350 to make $110, representing a 31% return on capital at risk. But proper position management can achieve win rates between 60-70% and make the strategy profitable over time despite the unfavorable risk-reward ratio on individual trades. Here, you do not have to guess the direction of the underlying; simply position for an interval of price variation.

When to Enter Iron Condor Trades

Timing your entry separates the increasing chance of having a profitable iron condor trade from frustrating losses. You now understand the mechanics of this four-leg strategy, but knowing when to deploy it determines whether you're selling options at optimal prices or entering positions that lack adequate premium.

High Implied Volatility Environments

Selling iron condors when implied volatility is elevated changes the entire profit equation. High IV inflates option premiums across all strikes and allows you to collect much more credit for the same strike width. You're selling lemonade on the hottest day when options are expensive. The increased extrinsic value means receiving larger upfront credits, which serves as your profit and cushion against adverse price movement.

Elevated IV increases option premiums on both the put and call sides of your iron condor. So you benefit from collecting richer premiums that create a larger margin of safety. You might collect $1.50 on a $5 wide spread during normal volatility. That same spread configuration might fetch $2.50 or more when IV spikes. This additional premium improves your risk-reward ratio without widening your strikes or accepting more risk.

The strategy capitalizes on volatility's tendency toward mean reversion. Volatility swings between periods of fear and complacency but drifts back toward its historical average over time. You position yourself to profit as volatility contracts and option prices decrease when you sell iron condors during elevated IV periods. This Vega component adds another profit driver beyond time decay.

Using IV Rank to Time Your Entry

IV Rank provides the context you need for intelligent entry timing. This metric scores current implied volatility from 0 to 100. Zero represents the lowest IV level over the past year and 100 represents the highest. A reading of 50 places you in the middle of the yearly range.

The practical threshold sits above 50 or 70 on the IV Rank scale. Option premiums are inflated relative to their historical range when IV Rank exceeds these levels. I look for opportunities above the 60 mark when selling iron condors, as this signals that current volatility sits in the upper portion of its annual range. A subsequent drop from IV Rank of 70 to 50, for example, produces significant profit from the Vega component alone!

High IV Rank often indicates potential overpricing of options. Comparing the current IV against its one-year range gives you a quick read on whether you're receiving fair compensation for the risk undertaken. On top of that, high IV Rank environments see accelerated theta decay in dollar terms because the original premium is higher.

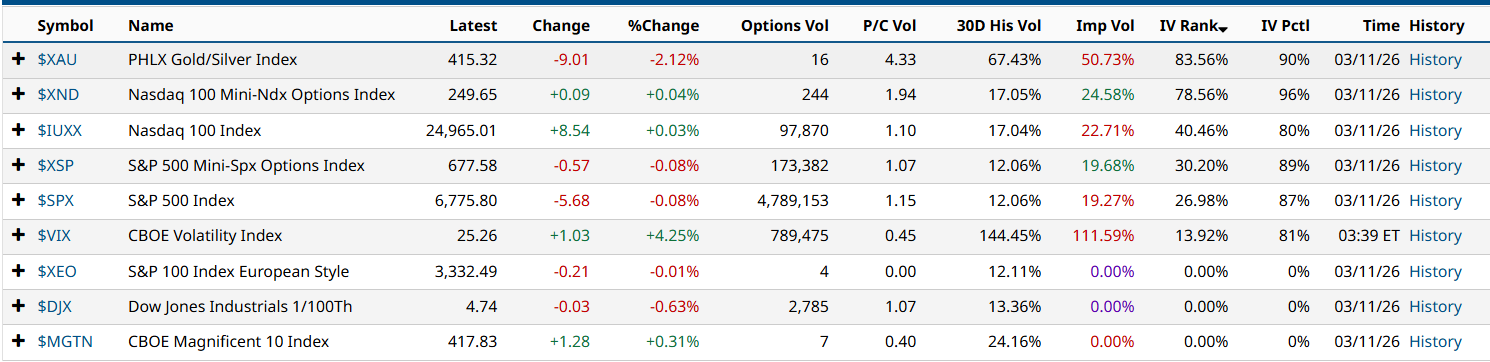

Below you have a table from Barchart.com where I screened only Indexes. NASDAQ should be a good candidate to open an Iron Condor at this moment....

Ideal Market Conditions for Iron Condors

Range-bound price action is the foundation for successful iron condor trading. I need the underlying asset to trade within a specific range, between key technical levels like the 50-day and 200-day moving averages. I prefer to use Support and Resistance lines, which work well enough to position the short strikes of the Iron Condor. Stocks combining after significant moves or trading in established channels present suitable opportunities.

The sweet spot combines elevated IV with expectations for price consolidation. You want high premiums from volatility while anticipating the stock will settle into a range. Conditions align for deploying this strategy when price action is expected to consolidate and no major news events threaten to break the range.

Avoid iron condors when expecting significant directional moves, during periods of extreme volatility expansion, or ahead of major announcements that could cause large price swings. Entering trades in low IV environments undermines the strategy because thin premiums offer insufficient compensation for the risk. From a theoretical point of view, you should target expirations between 30 to 45 days to balance premium collection with time decay acceleration for time frames. I prefer to use longer expirations and use another way to trade Iron Condors.

Step-by-Step: How to Construct Your First Iron Condor

Constructing your first iron condor requires systematic execution through six distinct steps. Each decision point affects your probability of profit and risk exposure, so precision matters more than speed.

Step 1: Select the Right Underlying Asset

Choose a stock, ETF, or index with low expected volatility to start. Your target universe becomes liquid options with tight bid-ask spreads and high open interest. Range-bound stocks with stable price action and sufficient liquidity present ideal candidates. Broad ETFs like the SPY or large, active stocks meet these criteria and offer the consistent price behavior necessary to execute directionally neutral strategies. Assets with upcoming earnings announcements or major catalysts that could trigger breakout moves should be avoided.

Step 2: Choose Your Expiration Date

Target expirations ranging from 30 to 45 days to establish a balance between profit potential and time decay. This timeframe allows theta to accelerate without excessive exposure to sudden price movements. Options with up to two weeks to expiration decay faster but increase vulnerability to price swings. Options with 60 or more days to expiry experience slower time decay while becoming more sensitive to volatility changes. Shorter-term options have smaller premiums due to less time value but carry heightened gamma risk.I prefer to trade longer-dated option expirations like 70-90DTE because they give a better edge and deliver more consistent results. The Pro Iron Condor we trade is one example.

Step 3: Select Strike Prices at Proper Delta

The delta column in your options chain shows what you need. A common target sits around 15 to 25 delta for your short strikes. A 20 delta translates to a 20% statistical chance the option finishes in-the-money. Some traders sell options one standard deviation below and above the current price, while others use two standard deviations for even higher probability trades. A short contract with a 0.05 delta represents two standard deviations and indicates a 95% probability of expiring out-of-the-money. But these type of selection can make you win a lot smaller amounts and lose big in a single trade. Technical analysis helps determine ideal strikes by identifying support and resistance levels.

Step 4: Calculate Net Credit and Risk

Your net credit represents maximum profit potential. Common practice targets one-third of the wing width. If your wings are $5 wide, collect $1.66 in credit. Another approach targets 50% of the spread width - but this will bring a not wide enough Iron Condor that may lead to constant adjustments. The maximum loss equals the spread width minus the credit received. If you sell a balanced iron condor with $5 wide wings for a net credit of $1.64, the maximum loss reaches $336 per contract. In summary, Risk vs Reward needs to be balanced according to your risk tolerance.

Step 5: Execute the Four-Leg Trade

Enter this as a single multi-leg order using an "iron condor" order type. The market moves fast. Executing all four legs at once locks in one price for the entire bundle and controls slippage. Limit orders manage costs and ensure execution at desired prices. Legging in separately creates directional risk and skews your breakeven prices. If you are using longer dated options (80-90 DTE), you can enter each leg separatly, especially if the full Iron Condor is not willing to get filled. On this longer dated options price variation will not impact options prices as 30-40DTE.

Step 6: Set Your Profit Target and Stop Loss

Close the position when it captures 30-50% of maximum profit. Stop losses help limit downside if the underlying moves against your position. Think over attaching a stop-loss order to manage risk exposure. Account size and risk management strategy must accommodate the maximum potential loss associated with the position.

Managing Your Iron Condor Position

Opening an iron condor position represents just the beginning of your trade... What happens after entry determines whether you capture consistent profits or watch winning trades deteriorate into losses. Active position management separates traders who achieve consistent results from those who struggle with this strategy.

When to Take Profits (The 30% Rule)

Close your iron condor when you capture 30% f the initial premium collected. This ensures more consistency over time. You received $1.00 in credit? Exit when the position value drops to $0.60 or $0.70. Some traders prefer the more aggressive and exit at 50% profit target. This increases exposure even further. This approach frees up capital for new trades and avoids the risk of late-stage reversals.

Holding positions until expiration increases vulnerability to unexpected price movements during the final days. Taking profits early changes the strategy from a high-probability gamble into a systematic income approach. Time decay accelerates near expiration. But so does gamma risk. This makes early exits the prudent choice.

Monitoring the Untested Side

Research shows that adjusting the untested side works better than modifying the tested side. The underlying price approaches one short strike? The opposite spread loses premium faster due to theta decay and favorable price movement. Rolling this untested side closer to the current price collects additional premium that offsets potential losses on the threatened side.

The stock moves upward toward your short call? Your put spread becomes the untested side. Rolling the put spread to higher strikes brings in extra credit. This widens your breakeven points and increases total premium collected. This attacking adjustment repositions your profit range and maintains defined risk.

Adjusting Based on Price Movement

Adjust when the underlying touches a short strike or when the short option reaches 0.30 to 0.40 delta. These mechanical triggers remove emotion from adjustment decisions. Rolling the untested side at 45 days to expiration when one side is tested with more than 30 days remaining captures profit from the safer spread.

Defensive adjustments involve rolling the threatened side itself. Though this functions as loss mitigation rather than profit enhancement. Sometimes buying back the threatened side minimizes losses if you believe the stock is breaking out of its range.

Rolling Strategies for Extended Time Frames

Rolling the entire position to a later expiration extends trade duration and widens breakeven points. This strategy works when you maintain confidence in the price range and view current movements as temporary. Close the existing position and reopen it at a later date. Do this for a net credit.

Rolling in-the-money spreads for a credit proves difficult or impossible. The farther from expiration, the less time value remains in ITM spreads. Rolling repeatedly while the stock moves against you increases risk rather than reducing it.

Iron Condor Adjustments and Risk Management

Adjustments aren't optional when trading iron condors. The underlying asset will test your strikes, and your response determines whether you preserve capital or accept maximum loss. Specific adjustment techniques address different scenarios, each with distinct risk implications.

Rolling the Untested Spread Closer

Rolling the untested side stands as the most classic adjustment in iron condor trading. Price moves toward one wing and the opposite spread sits far out-of-the-money with minimal value remaining. Closing this safer spread and reopening it closer to the current price brings in additional credit that reduces your overall position risk.

But this approach exposes you to whipsaw risk if the stock reverses direction quickly. The trade-off proves worthwhile because reducing risk takes priority over avoiding reversals. I collect extra premium that widens my breakeven points while maintaining defined risk parameters.

Converting to an Iron Butterfly

An iron butterfly adjustment repositions your entire trade around the current price. You move the untested side closer until both short strikes meet at the same level. This creates a tighter profit range but increases reward.

The adjustment works when you want to shift from defense to offense and center your position on where the stock trades now rather than where it started. You can widen the breakeven point, increase profit, and reduce risk depending on the adjustment strategy. The conversion transforms your neutral range trade into a more focused bet on price stability at the current level.

When to Cut Losses and Exit

Set your maximum loss before placing the trade. A reliable stop loss sits at two to three times the credit you received. If you collected $0.50 in premium, exit when the unrealized loss reaches $1.00 with a 2x stop or $1.50 with a 3x stop. Use the lower multiplier for smaller accounts or when taking a cautious approach.

Exit decisions require evaluating time remaining, loss multiple, gamma exposure, volatility changes, and assignment risk. Sometimes a clean exit preserves more capital than attempting repairs, especially when you have the short strike deep in-the-money near expiration.

Managing Gamma Risk in Short Time Frames

Gamma accelerates as expiration approaches and makes your position increasingly sensitive to price movement. Under 30 days to expiration, seriously think about exiting the position. If you opened trades with approximately 40 days remaining, treat 20 days left as a critical checkpoint. Option Greeks react violently to small moves in the underlying during these final weeks. Combined with a thinner time value, you face large P&L swings from relatively minor price changes.

Common Mistakes Trading Iron Condors

Despite iron condors appearing straightforward, specific mistakes drain accounts. You need to understand these pitfalls before they cost you capital. This separates sustainable traders from those who abandon the strategy after repeated losses.

Opening Trades in Low IV Environments

Low implied volatility undermines the entire strategy when you enter iron condor positions. Low IV markets compress premiums and force you to accept pennies for strikes that aren't far out-of-the-money. Your short options increase in value once volatility expands, even if the underlying price remains unchanged. This creates losses without directional movement. Volatility tends to cluster, so low IV environments often persist. When the inevitable spike arrives, it hits hard. The profit zone narrows when premiums are thin and leaves insufficient compensation for the risk undertaken.

Using Short Time Frames Without Protection

Zero-day-to-expiration trades and weekly iron condors expose you to extreme gamma risk. Pin risk becomes a real threat as even out-of-the-money options can trigger assignment during after-hours trading. Spreads on low-volume underlyings become difficult to buy back near expiration and potentially trap you in positions as the Greeks turn violent. You'll find it challenging to close all four legs of an iron condor on expiration day, even for high-volume tickers.

Ignoring the Greeks (Delta, Theta, Gamma, Vega)

Unexpected losses result when you fail to monitor delta and theta values. Delta measures price sensitivity while theta represents the time decay rate. Both require regular assessment. Vega risk means your position loses value when IV spikes, creating losses even when the underlying hasn't breached your short strikes. So you accept negative gamma risk in exchange for positive theta profit, a trade-off that demands constant monitoring.

Holding Until Expiration Without a Plan

The perception of iron condors as a set-and-forget income source proves dangerous. Assignment risk escalates when short strikes go in-the-money near expiration, especially with little extrinsic value remaining. Clear exit strategies protect capital and minimize adverse market impact.

Overleveraging Your Position

You increase vulnerability to market swings when you allocate more than 3-5% of your portfolio to a single iron condor. A high win rate doesn't guarantee long-term profitability if the few losing trades aren't managed right. The most common mistake involves conflating high probability of profit with positive expected value.

ADVANCED: Unbalanced Iron Condors

Standard iron condors maintain equal wing widths on both sides and create a neutral directional stance. Unbalanced iron condors break this symmetry and introduce directional bias while preserving defined risk. This variation suits scenarios where you lean bullish or bearish but still want range-bound profit potential.

You need to widen strikes on one side of the trade to create the skew. Expand your put spread width for bullish positioning. Sell the $45/$40 puts on a $50 stock rather than the $45/$44 puts. This transfers risk to the downside and removes risk from the upside, creating positive delta exposure. Bearish skew works inversely by widening call strikes.

You can also trade different quantities on each side. A bullish setup might involve 10 put spreads paired with only 5 call spreads. This approach generates delta of 24 and delta dollars of 9,379 in practical application. Capital at risk increases compared to balanced structures, from $7,600 to $8,120 in tested examples. Return on capital decreases from 31.58% to 23.15%.

Maximum risk equals the width of your widest spread minus the credit received. A $2 wide spread collecting $0.80 credit caps losses at $1.20. Both breakeven calculations follow standard iron condor formulas and add or subtract the net credit from short strikes.

Skewed positions respond negatively to implied volatility increases because you remain net short premium. Deploy unbalanced iron condors during elevated IV environments.

Conclusion

You now have the framework to trade iron condors profitably. The strategy delivers consistent results when you enter during high IV environments, construct positions with proper delta targeting and do not manage them until expiration.

Note that your success hinges on disciplined position management. Take profits at roughly 30% of maximum credit, adjust the untested side when threatened and never overlook the Greeks. Avoid overtrading or entering when premiums are thin.

Start small, track your results and refine your approach. Become skilled at these principles, and iron condors will become a reliable income generator in your trading arsenal.