- May 3

Why I Trade 90–120 DTE Options Instead of 0DTE — And What the Results Show

- Pedro Branco

- 0 comments

By Pedro Branco | MyOptionsEdge

Every week, someone in the options trading community shares a screenshot of a 0DTE trade that made 200% in a morning. The comments fill up fast. People ask which broker, which strike, which time of day.

Nobody posts the screenshots from the other days.

I've been trading SPX options professionally since 2020 and teaching options for more than 10 years. I don't trade 0DTE. Not occasionally. Not as a small allocation. Not at all. And the performance record of my live fund, +270% since January 2022 compared to SPX +43% over the same period, was built entirely without touching a single zero-day-to-expiration contract.

This post isn't another warning about 0DTE risks. There's already plenty of that written, including my earlier post on why I avoid 0DTE. This post is a direct, practical comparison between the two approaches: what each one actually looks like in practice, what the structural differences are, and what the numbers show when you run both for long enough to matter.

What you'll learn in this post

The structural difference between 0DTE and 90–120 DTE options; not in theory, but in terms of how they behave in your account

Why gamma is the hidden variable that determines which approach survives long-term

The theta decay curve that most 0DTE traders have never seen, and what it actually means for premium sellers

How 90–120 DTE gives you something 0DTE can never provide: the ability to manage your way out of a bad position

My account's actual results, and what they demonstrate about consistency vs. excitement

The core difference: you're playing two completely different games

When traders compare 0DTE to longer-dated options, they usually focus on profit potential. That's the wrong frame. The more important difference is structural. How the two approaches behave mathematically, and what that means for your ability to trade consistently over time.

0DTE options are a prediction instrument. Every 0DTE trade requires you to be right about direction, magnitude, and timing: all within a single trading session! The leverage is extreme. The feedback is instant. And the gamma exposure means that even small moves against you can destroy a position's value in minutes.

90–120 DTE options are an income instrument. You are not predicting direction if using the proper strategies. You are collecting premium and giving the position time to work. Time during which the market can move against you, stay flat, or recover, and you still have room to manage. The leverage is controlled. The feedback is slow and deliberate.

These are not two versions of the same activity. They are fundamentally different approaches to the market.

The gamma problem — and why it's 50x worse than most traders realise

Gamma measures how quickly delta changes when the underlying moves. In plain terms: high gamma means your position's risk can change dramatically from one minute to the next.

For a 0DTE option, gamma can be up to 50 times higher than for a 45-day option at the same strike. This is not a small difference. It means that a 1% move in SPX, entirely routine on any given day, can cause your 0DTE position's delta to shift by an amount that would take weeks to develop in a 60-day position, for example.

Here's what that looks like in practice. Imagine you open a 0DTE iron condor on SPX at 9:45am with what appears to be a comfortable range. By 11:15am, a Fed official makes an unscheduled comment. SPX moves 0.8% in four minutes. Your short put delta, which was 0.10 at entry, is now 0.45. The spread that was worth $2.10 in credit is now showing a $4.80 unrealised loss!

You have approximately four hours left in the trading day. You can close at a loss, roll at an even worse price, or hope the market reverses. There is no fourth option.

This scenario happens to 0DTE traders constantly. It's not bad luck. It's the mathematical consequence of the gamma profile you accepted at entry.

The theta decay curve nobody shows 0DTE traders

Here is the insight that changes how most traders think about time decay. And why it's directly relevant to the 0DTE vs. 90–120 DTE comparison.

Most options education teaches that theta decay accelerates near expiration. This is true for at-the-money (ATM) options. But for out-of-the-money (OTM) options, the ones most premium sellers are actually trading, the decay curve looks completely different.

OTM options decay fastest between 100 and 30 DTE. In the final 30 days, OTM options have already lost most of their time value. The remaining theta is thin. The gamma is now high. You are taking on more risk for less reward.

This is the mathematical case for 90–120 DTE that almost no one explains clearly:

You are collecting the most theta per unit of gamma risk when you are in the 90–120 DTE window. By the time you reach 30 DTE, the ratio has flipped — you're carrying significant gamma for diminishing theta returns.

This is why I typically close my positions before 30 DTE. Not because I'm being conservative. Because the trade has already done most of what it's designed to do, and continuing beyond that point changes the risk profile in a way that doesn't serve the income objective.

A 0DTE trader is operating entirely in that unfavourable zone with maximum gamma, minimum theta, maximum prediction requirement. Every single day!

What 90–120 DTE actually gives you: room to manage

The most underrated advantage of longer-dated options is not the better theta/gamma ratio. It's something more practical: the ability to manage your way out of positions that move against you.

When I open a new SPX Best position at 90 DTE with the short strikes positioned below multiple support levels, here is what I can do if the market moves against me:

Adjust the delta by modifying one side of the structure, collecting additional premium while rebalancing the position

Roll the position further in time if needed, extending DTE and resetting the theta clock

Tighten or widen the structure based on where SPX is trading relative to support

Simply wait, because at 90 DTE, a 2% move against me is not an emergency. The position has weeks to recover or stabilise before I need to act decisively

None of these options exist meaningfully in a 0DTE context. You cannot roll a 0DTE trade into a more favourable position at 3pm. You cannot wait for the market to stabilise. The day ends in a few hours. Your adjustment toolkit is nearly empty.

This is not a minor difference in tactics. It's the difference between a trading approach that rewards skill, patience, and risk management — and one that rewards luck and speed.

A direct comparison: what a year of each approach looks like

I want to be specific here, because the comparison between 0DTE and 90–120 DTE often stays abstract. Let me make it concrete.

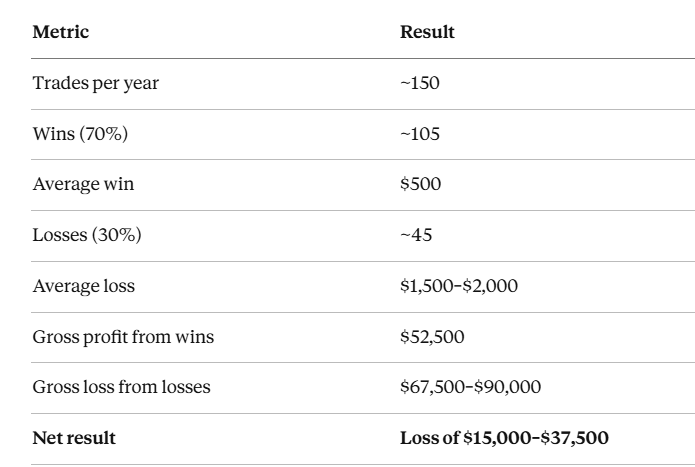

The 0DTE trader's year (realistic, not worst-case)

A trader running 0DTE iron condors on SPX, 3 days per week, targeting $500 per trade with a 70% win rate and typical losses of 3–4x the credit collected:

The 70% win rate sounds excellent. The problem is the asymmetry: one bad day in a 0DTE trade doesn't just erase a week of profits. With the gamma exposure described above, it can erase a month. The traders who post the winning screenshots are real. So are the losing days. They just don't make it to social media.

The 90–120 DTE trader's year (based on SPX Best historical data)

Running the SPX Best strategy with typical parameters, 2–3 simultaneous positions at different expirations:

Fewer trades. Higher win rate. Better risk management. Significantly better outcome.

The 0DTE approach requires you to be right 3 times a week, every week, all year. The 90–120 DTE approach requires you to be right on position sizing, entry conditions, and adjustment timing, over a 4–6 week window per trade. That's a fundamentally more manageable cognitive and emotional challenge.

"But 0DTE traders make money too"

This is true, and I want to address it directly rather than dismissing it.

Some 0DTE traders are consistently profitable. They tend to share three characteristics: they trade very small size relative to their account (so individual large losses don't matter), they have extremely well-defined rules that remove emotional decision-making, and they have been doing it long enough to have experienced (and survived) multiple extreme gamma events.

If you have the discipline, the account size, and the years of experience to trade 0DTE this way, it can work. But I would argue that those same qualities (discipline, rules, experience) applied to a 90–120 DTE framework produce better risk-adjusted returns with less stress and less account volatility.

I am not saying 0DTE traders are wrong. I am saying that if you are choosing between the two approaches, the structural evidence strongly favours the longer timeframe, especially for traders who want consistent income rather than occasional spectacular wins.

The psychological dimension: what your trading actually feels like

This is the part that doesn't appear in backtests. After 15+ years trading options and watching hundreds of traders learn these strategies, the psychological difference between 0DTE and 90–120 DTE is one of the most significant practical factors.

0DTE trading is high-frequency, high-stress, and emotionally exhausting. You are making decisions every hour. Every move in the underlying requires an assessment. You are constantly monitoring, constantly exposed, constantly one bad candle away from a position emergency. Traders who do this for months without proper mental preparation burn out, or blow up, regularly.

90–120 DTE trading is calm, deliberate, and sustainable. After opening a position, I spend 15–30 minutes per day monitoring. Most days, nothing needs to happen. The position does its job. I review the Greeks, confirm nothing has approached my adjustment triggers, and move on. The stress level is qualitatively different. And that difference directly affects the quality of my decision-making over time.

Consistent trading income is not built in a single dramatic session. It's built through hundreds of unremarkable days where discipline held, risk was managed, and the strategy was trusted to do what it was designed to do.

How I use 90–120 DTE in practice: the SPX Best and Ride Trade

My two primary strategies both use longer-dated options for the reasons described above.

The SPX Best uses 80–100 DTE on SPX put options in a broken wing butterfly structure. The position is opened with short strikes positioned below multiple technical levels, giving the trade a wide buffer before any adjustment is needed. The average position is open for 6-8 weeks and closes at a profit target of 10–15% on capital.

The Ride Trade uses 80–140 DTE on SPY options in a calendar spread structure. The longer DTE on the Ride Trade serves a different purpose: the calendar spread benefits from the difference in theta decay rates between the two expirations, which requires sufficient time for that differential to express itself. Short-dated calendar spreads produce thin returns relative to their risk.

Both strategies were designed around the theta/gamma relationship described in this post. The DTE choice is not arbitrary or conservative by default. It's the mathematically optimal window for the type of premium collection these strategies perform.

My account's track record: what 90–120 DTE actually delivers

Since January 2022, through the 2022 bear market, the 2023 recovery, the volatility spikes of 2024, and into 2025, the fund has returned +270% compared to SPX +43% over the same period.

This was not achieved by predicting market direction. It was not achieved by identifying the right moment to buy calls or puts. It was achieved by running structured, longer-dated, non-directional positions that collected premium, managed delta, and closed at profit targets. Consistently, month after month.

The full monthly performance record is publicly available on the Trading Account page. Every trade, every month, since we started. No cherry-picking. No hindsight.

Key takeaways

0DTE options require directional prediction, create extreme gamma exposure, and give you no room to manage positions when the market moves against you. The theta/gamma ratio at zero DTE is the worst it ever is across the option's lifetime.

90–120 DTE options collect premium during the period of maximum theta-to-gamma efficiency for OTM options, give you weeks to manage and adjust positions, and produce a trading experience that is sustainable, lower-stress, and compatible with consistent income generation.

The results speak clearly. The SPX Best strategy, built on 70–90 DTE structures, has delivered an 83% win rate across 63 documented trades since October 2021. The fund's overall +270% return since January 2022 was built without a single 0DTE trade.

If you are currently trading 0DTE and struggling with consistency, or if you're evaluating which approach to build your strategy around, the data and the structural logic both point in the same direction.

Want to follow these strategies live?

Every SPX Best and Ride Trade position I open is posted in the Trading Room in real time and at the Trading Community, the entry rationale, strikes, payoff diagram, brokerage screenshot, and every adjustment as it happens.

If you want to see how 90–120 DTE options management works in practice, not in theory, not in a simulation, but in real market conditions with a real fund, the Trading Community is where that happens.

👉 Start your 15-day free trial — full Trading Room access, live SPX Best and Ride Trade positions, weekly IV research. No commitment, cancel anytime.

Or read more about the specific strategies:

→ The SPX Best Options Strategy — 83% win rate, 70–90 DTE broken wing butterfly on SPX

→ The Ride Trade — calendar spread income strategy on SPY

→ View the full account performance record — every trade documented since January 2022

Disclaimer: Past performance is not indicative of future results. Options trading involves significant risk and is not suitable for all investors. All performance data shown is from a real account and is publicly documented on the Trading Account page.

About the author: Pedro Branco is a volatility-focused index options trader who has traded options for more than 15 years and has run a live investment fund since 2020. His fund uses exclusively longer-dated, non-directional strategies — the SPX Best and Ride Trade — with results published monthly and available for public verification. He is the author of The Volatility Trading Plan, available on Amazon.