The Iron Condor is a neutral options trading strategy designed to profit when the underlying asset stays within a defined price range until expiration.

It is created by combining a bull put spread and a bear call spread, which produces a limited-risk, limited-profit trade that benefits from time decay (theta) and relatively stable markets.

Market outlook: Neutral / range-bound

Maximum profit: The net premium received

Maximum loss: Defined and limited

Ideal environment: Low to moderate volatility markets

Best underlying assets: Indexes like SPX or highly liquid stocks

Traders often use Iron Condors because they:

Generate consistent premium income

Have defined risk

Benefit from time decay

Work well in sideways markets

Iron Condors: What are they?

One of the most discussed selling options trading strategies is the Iron Condor. In short, it is composed of 2 sold Vertical Spreads (Credit Spreads) out-the-money: one Short Put Vertical and another Short Call Vertical that delivers a credit (cash received in the brokerage account). Usually, the sold strike prices of each vertical can be defined at 10 or 20 Delta (as examples of wide iron condors). This will deliver probabilities of profit at the expiration of 80% to 90%. The total credit of the sold options contracts is the maximum profit for the Iron Condor. But, as you may imagine, the high probability of success also delivers a higher risk. This sounds very attractive, but it is dangerous to understand this strategy in this simplistic way! An iron condor is a delta neutral strategy (a type of trade that I like) that profits the most when the underlying asset does not move much, which means it trades in a range. Although the trader can open the iron condor with some directional bias (bullish or bearish).

In options trading, nothing is easy and straightforward. There are several dimensions (options are a multidimensional space) to take into consideration – not only price movements... as in stock trading.

Despite the attractive potential return of the Iron Condor strategy, this is not structurally built in the trader advantage, especially if done in shorter time frames and the options selected are under low implied volatility. In fact, it presents lower attractive ways to adjust or repair when the price of the underlying moves against it. Because Iron Condors are placed in less than 45 DTE, as advocated by many instructors (or even content websites - sorry to not reveal, but it will be very easy to find a website that defends Iron Condors to be placed in the lower short-term than in longer-term, because of the attractive high Theta). But, at shorter time frames, Gamma enters the equation, and is difficult to control the t0 line, maintaining it flat (Gamma is the enemy of any Delta Neutral options trader). Although attractive when they are opened, the iron condor opened, easily can turn into fast losses with low alternatives to adjust. One relevant variable that is also neglected when discussing Iron Condors is Vega. Although Vega can be similar between shorter and longer time frames Iron Condors, the faster reaction of shorter time frame IV to any spike can be brutal, turning impossible to recover or even repair the Iron Condor. Finally, shorter time frames have a less attractive risk/reward structure.

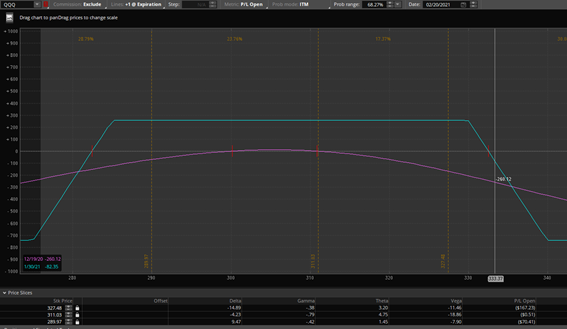

Iron Condor Example

Below, is an example of an Iron Condor on QQQ with 40 DTE and sold strike prices at 20 Delta for each credit spread, where the the current price is $311. Its maximum profit is the total credit received (in the image below is $275). But, this is the maximum profit potential. Experienced traders do not leave this position until expiration. Usually, they define the potential profit of this type of trade from 25% to 40%, depending of their risk tolerance.

On the risk side, this is a limited risk strategy. In the example, it is $735, which is the maximum loss this trade can deliver.

You can easily understand by looking at the graph above the pros and cons of this trade.

If the stock remains within a certain trading range during the holding period, it can generate a nice profit, based on the invested capital (maximum risk of the trade). If we look into Greeks, my beloved Delta/Theta ratio is not the best when compared to the Ride Trade or the SPY Speed trade (even Gamma is high enough at this point of the trade). Additionally, if there is an IV spike due to a fast move down, the t0 line moves low and turns almost impossible to adjust or recover.

You can also see what happens if the QQQ price moves fast in one direction: the losses start to appear and, if that movement continues, they increase fast due to higher and higher Gamma as long as the price is moving towards one of the sold options strike price. You can understand this effect by computing the slope of the t0 line (magenta line in the graph).

15 days after the same Iron Condor appears like this, where the t0 line is steeper (means high Gamma) near the short strike prices than it was when the trade was entered.

Iron Condor adjustments (or repair strategies)

Now, let’s focus on alternatives to adjust this Iron Condor trade in case things start to move against it. In fact, this trade offers low alternatives for repairing. Unlike other strategies that I trade this one could simply go wrong and could be difficult to recover from a big loss.

There are 2 main repair trades for Iron Condors. The first and more obvious is when the price starts to approach one of the sold options strike prices the trade can simply buy back at a profit on the opposite side and sell to open a new Vertical closer to the stock price (could be again at 20 Delta) for additional credit. This shrinks the price interval, and we lower the initial probability of profit and for sure this credit is not compensating the loss on the “touch” side Vertical. The second is to move the whole structure (with possible adjustments in sold strikes) further in time for additional credit. But this will reduce Theta of the whole trade and more time to get in profits and if the price continues to move against, the trade continues to lose…

So, there is no big flexibility to adjust or repair this kind of Iron Condor in an easy and straightforward way. At least if you enter Iron Condors when the underlying:

1. … has options under a low Implied Volatility;

2. … you open the position in short time frames.

When trading Iron Condors you need to have a plan to adjust them in case the underlying stock or index will make a big move in either direction.

The decisions of when and how to adjust should all be part of your trading plan and you should know in advance what you are going to do should a big move occur.

What you don’t want to do, is close your eyes, cross your fingers, and hope that the position comes back into profit.

In a common Iron Condor, the maximum loss is more than the maximum gain, so it is key that you don’t let small losses turn into very big losses because they are difficult to recover. Under the Pro Iron Condor strategy, you can learn several ways to adjust Iron Condors in order to have them always in your favor and cut down potential high losses. Remember that a trader should cut losses and leverage profits. This is much easier said than done. That is why we need a proper plan and take decisions that maximize profits and minimize losses.

When to enter an Iron Condor?

But there are better conditions when entering Iron Condors to increase its success odds. Remember this is a Vega negative trade, which means we are selling volatility (this strategy is based on selling options). Hence, when IV is high the trader gets a higher credit and the Risk /Reward of this strategy greatly improves. Most options traders base their decision to enter this trade because they think the underlying price will remain in the structure positive range. This is not the right approach! What they will soon learn is that any underlying can move fast in either direction and/or IV can increase and losses start to get bigger …

Traders should not base their decision to enter an Iron Condor position on the underlying’s price interval. Instead, they should consider primarily the implied volatility level! If Implied Volatility is relatively high and soon the trader expects it to decrease, this will increase greatly the odds of getting a profit in this strategy. At high IV the max credit received is higher and the max risk is lower. Again, as I am always saying when trading options, Implied Volatility is key (although there are other dimensions to take into consideration) by opposition to the stock trader where the price is the only variable that matters.

After a stock or ETF has a big period of price increase, usually comes a period of a down move, as you understood from your experience there are price cycles. This impacts the implied volatility (it starts to increase) of its option premium and it’s when Iron Condors increase their odds of success.

Sometimes, news can impact also implied volatility, like earnings announcements. Since these are short Vega trades and the trader is selling volatility, it increases the odds of success to open trades when implied volatility is high. Sometimes, there is also fast price recover, which the iron condor trader does not want, but they are combined with decreasing implied volatility and usually, the trade can present small losses or even show profits.

But how to check if the Implied Volatility is high or low? For SPY, for example, an IV of 35% is pretty high, but for TSLA is very low…the answer to this question is to check the IV Rank.

Through the use of this indicator, the trader can determine whether the implied volatility is high or low relative to what it was in the past and even relative to other options. The way it works is that an option’s current implied volatility is compared against the historic range of implied volatilities for that option (usually in the past year).

As an example and a rule of thumb, an IV rank above 50-60 is considered high. So, it is a good environment to enter an Iron Condor. I have the code for the IV Rank indicator for ThinkorSwim that you can ask from me. Just email me requesting it and I am happy to send it to you.

As you understood from my initial description, I prefer to open long-term iron condors to short-term condors. The base for this decision is the flexibility of their adjustments (that shorter-term ones do not allow) as well as a lower number of adjustments needed. The trader is much more defended in case of any fast movement of the underlying. And, yes, they deliver lower profitability in a longer time frame but they are much more (and I can say, much, much more) consistent in terms of results. The traders in our community understand what I am saying due to our very good experience with the Pro Iron Condor strategy I developed and we are trading. You can tell me now that time decay (or Theta decay) is lower on longer-time frames and I agree with you, but my experience is that is preferable to have a consistent income of 10% a month than having 25% a week with some weeks losing 50% or more..

Everyone has their own preference and trading style, but for me, which privileges steady income and consistency, I find long-term condors better. Additionally, positioning the trade is a way that simplifies adjustments, and knowing exactly when to exit is key. Not to wait for the max profit. And some of my students after some months start to agree with me!

Why does Contango or Backwardation of options chain matter?

Another characteristic of option Implied Volatility that matters when discussing shorter-term and longer-term Iron Condors is the status of the IV on the options expiration. They can be in Contango (under a low volatility environment, which is a normal state and should be under this status majority of the time – let’s say 80% or more) and Backwardation.

Contango and Backwardation refer to the shape of the implied volatility term structure. When shorter-term options chains have lower implied volatility and, hence, longer-term options expirations have higher average implied volatility, we say it is in Contango. This is a normal state because, as you may understand, as far out as we are in time, there are more uncertainty and volatility traders are willing to pay an extra premium.

The opposite occurs when the underlying experiences a fast drop in price or there is higher uncertainty due to earnings announcement. The volatility in the front months skyrockets while the back months don’t rise as much. This is because the market knows that panics usually die down within a few weeks and things return to normal. This is called backwardation in implied volatility. When this happens, we can be a bit more aggressive in choosing shorter-term months, but we never know. Even under these Backwardation moments, longer-term options offer a nice opportunity because they are also impacted by the rise in Implied Volatility.

How to approach Iron Condors the best way

Since there was high interest in our community to trade this strategy, I researched a lot under several market conditions and found out that the best way to trade Iron condors is using higher time frames. The Pro Iron Condor strategy is a new approach to trade Iron Condors that maximizes consistency and describes how to overcome its negatives. As you know, I like to manage risk using Greeks and I always think outside the box. The results of the research were so promising that I have included this new strategy in my portfolio. Please, be cautious when trading Iron Condors using the free information over the web! Without an analysis and hypothesis testing, I am not putting my money into any strategy.