Originally published on 2023 · Last updated April 2026

OTM options decay fastest between 100 and 30 DTE — not in the final 30 days. The time decay curve most traders have never seen, with SPX and SPY real examples.

Time decay is the price erosion of an options contract (either a Put or a Call). Any long options holder must take into consideration this effect. As time passes, an options contract loses value. In generic terms, time decay accelerates as the option approaches its expiration date, where the option contract is exercised (if it expires in-the-money) or expires worthless (if out-the-money). Is there anything the trader can do to avoid time decay in options? Yes, there is. Time decay in options is key in some options strategies I developed and its understanding is a must for any knowledgeable options trader.

Theta is the option Greek that expresses an option's expected price variation with the passage of time (you can read more about the Greeks). Options are "decaying" assets. This means they lose value over time putting pressure on their "long" owners. Being an option buyer, the trader is losing value from the passage of time. On the contrary, the option writer (or option seller) is benefiting from time passage. Option prices decrease over time. An option's Theta estimates how much an option's price will decrease by each day that passes (with other variables constant - price, volatility, etc). The Greek Theta is always negative to the owner of long options contracts and therefore, option buyers must consider this losing effect on their strategies. On the contrary, the option writer (or seller) will have time decay on his side, having a Theta positive position. In fact, with these types of options strategies (my preferred ones), time is on our side. So, I am not stressed with the time passage. In fact, I want time to pass to benefit from options time decay... and expect to underlying does not move too much. These types of strategies, also called income options strategies, are the core strategies of my Hedge Fund.

I am sharing its trades with my Trading Community. Everyone is welcome to join and learn how to properly trade options, avoid rookie mistakes, ...

An option's premium (or the "options price") is composed of the sum of two key concepts that an options trader should master: Extrinsic and Intrinsic values. They are relative to the stock price the options relate to.

Intrinsic Value

The intrinsic value of an option (option premium) is defined by the difference between the underlying price (a stock or ETF) and the strike price of the option. As an example, in a Call option with a strike price of $40, and the underlying asset is trading at $50, the intrinsic value is $10. But, if we consider a Call with a strike price of $55, would have a “0” intrinsic value, because the Call option is “out-the-money”.

Extrinsic Value (or Time Value)

The extrinsic value of an option measures its “time value” or "time premium". As you may understand this is a metric that is more variable and depends strongly on the options implied volatility and time until expiration. But setting aside the effect of implied volatility, as much as we approach the expiration date, the extrinsic value will decrease as well as its rate of decay. If you buy a Call option with 30 DTE it will have a higher premium than the option at the same strike but with 7 DTE. This is easy to understand: as we approach the time to expiration date there is a lower probability of the long option owner becoming profitable (being “in-the-money” at expiration). Hence, the option's premium declines. Shorter-term options have higher decay than longer term.

Thinkorswim from Schwab can easily show for each option chain the Extrinsic and Intrinsic values. In the example below, you can see the 47DTE (AUG21) option’s chain where I highlighted three options:

1. 425 SPY Put (Out-the-Money) where the intrinsic value is null and, hence, it only carries extrinsic value, which is its full premium (or price) that in the example is 5.01;

2. 445 SPY Call (Out-the-Money), also carries only extrinsic value in the value of its premium (2.17).

3. 435 SPY Put (In-the-money) where the premium paid when buying it (7.96) carries both Extrinsic (6.33) and Intrinsic (1.63) values.

Below you have the comparison of three monthly options chains for SPY (136DTE, 47DTE, and 12DTE), taken from Thinkorswim platform that also can easily be configured to deliver the Greeks of each option at the time its current price was 433.72. Again, I highlighted the 430 Put on each option chain. We can easily conclude that Theta is increasing as we approach the expiration date. It starts with -0.06, moves to -0,08 and, at the 12DTE chain, it reaches the biggest value of -0,12. Note, that, as it is referred Theta is a negative value and represents the daily loss of the option. In this example, the SPY 430 Put that has a premium of 1.93 loses 0.12 per day (on average, giving other variables constant, like price and implied volatility).

Apart from impacts on Theta from Implied Volatility changes and other variables, I would like to focus this discussion on how option positioning (At-the-Money, In-the-Money, and Out-the-Money) affects Theta and hence the Time-Value erosion of its price.

This is very important to know because the majority of books and educational blogs on the web tell that the price decay of options accelerates in the last 30 days until expiration.

In fact, this is true, but is not the whole truth!

Sign up to receive my Weekly Market Outlook that includes Market Research, S&P 500 Quant Data, Fund Value, Promotions and more. Exclusive for subscribers

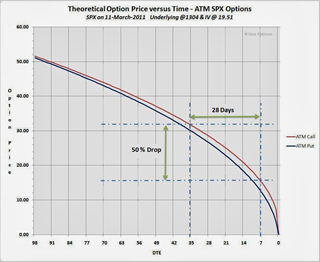

Below there is a graph showing the time decay for “At-the-Money” SPX options with theoretical option prices starting at about 100 DTE. Let’s divide the DTE (Days until Expiration) into 2 areas in the options decay curve: from 100-30 and below 30 DTE. You can easily conclude that time decay in the first interval, the curve is steady and slow, but below 30 DTE time decay accelerates (rate of time decay) and, in fact, circa 50% of the option value erases in this period!

In summary, we can say that ATM options have a faster decay as expiration approaches (mainly last 30 days).

Now, let’s analyze the same graph or options decay curve with a far “out-the-Money” option. The below graph shows the time decay curve for OTM 10 delta SPX options under the same period.

Surprise! it is basically the opposite! Note how much steeper the curve is for both calls and puts from around 100 DTE to around 30 DTE. This is the opposite of the ATM time decay! In fact, below 30 DTE the curve really flattens and time decay per day is very low. So, Selling Out-the-Money options in a short time frame is a beginner error!

OTM options have only "extrinsic value" and only this extrinsic value decays as time passes. An option's intrinsic value is the option's real value at any given moment, and intrinsic value does not decrease with the passing of time, by definition.

In essence, options that have the most exposure to decay are the ones with the most extrinsic value, which means that At-the-Money options deliver the greatest potential losses from theta decay. They have 100% extrinsic value and is where this is maximum!

Like most things in trading options, nothing is linear due to all variables that are changing every day that affect their pricing. Options are multidimensional assets and time is one of them. The decay rate of an option may speed up or slow down as time passes. This depends on whether the option is in-the-money, at-the-money, or out-of-the-money.

In generic terms, as expiration approaches: ATM option decay tends to speed up significantly, but OTM decay tends to slow down or maintain.

In fact, as seen by the options decay curves, the decay of at-the-money option prices accelerates as expiration approaches and gets closer. More specifically, the rate of at-the-money decay is fairly slow from 100 to 60 days to expiration. From 60 to 30 days to expiration, the rate of decay began to accelerate. In the final 30 days, the rate of decay really increases with the steepest decay occurring in the final 5-7 days.

As mentioned earlier, out-of-the-money options decay slower and slower as expiration approaches because near expiration, OTM options will be nearly worthless, which means the option doesn't have much to lose. For these options, the decay curve is steady in opposition to the ATM fast decay curve.

The front picture of this text illustrates the time decay of options across the options chain, as stated in the text.

Knowing these properties, we can really think about developing strategies. For example, if you have an options trade that is an ATM Calendars have the highest theta decay than OTM or ITM. ATM Short straddles have higher time decay than short strangles that are OTM… But, if you think on our strategies you can now see how they are developed to have an edge:

- The Ride Trade uses longer-term options and hence has more contracts with OTM options. It captures the steady low-time decay of those options where they decay the most. It is comprised of Calendar Spreads where the longer-term option is hedging the sold short-term option;

- The SPY Speed trade is using ATM options to collect its fast time decay. It uses a very short-term Calendar spread At-the-Money where time decay is maximum.

Now you can answer the initial question of this blog post: How to avoid time decay in options? Simply by choosing Theta positive options strategies! And being now a more experienced option trader, now you understand that the options decay curve is different in OTM and ATM options!

This is exactly why my fund uses 60–90 DTE options for the SPX Best strategy rather than short-dated contracts. The OTM decay curve shows that longer-dated OTM options decay steadily and predictably — which is what a structured, non-directional strategy needs. It's one of the reasons the fund has maintained an 83% win rate on the SPX Best strategy since 2021. You can verify the full performance record on the Trading Account page.

About the author: Pedro Branco is a volatility-focused index options trader with more than 15 years of experience and has run a live investment fund since 2020. The broken wing butterfly on SPX is his primary fund strategy, with results publicly documented since January 2022. He is the author of The Volatility Trading Plan on Amazon. Every strategy taught at MyOptionsEdge is actively traded in his fund.